Industry

Increase Profitability by 15-20 Basis Points by Increasing Pull-Through

.png)

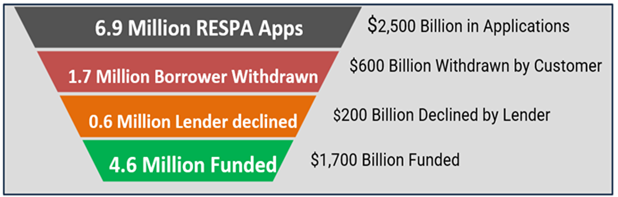

The latest HMDA data makes the scale of the fallout problem impossible to ignore. Industry‑wide, lenders took about 6.9 million RESPA applications representing roughly $2.5 trillion in requested mortgage credit, yet only about 4.6 million loans and $1.7 trillion in volume actually funded—meaning just 59% of applications converted to closed loans, barely six in ten.

Most of the gap came from borrowers themselves: roughly three‑quarters of loans that failed to fund did so because the customer chose to withdraw, not because the lender formally declined the file. The lender lost the gain on sales and fees from a closed loan AND the lender spent $700–2,000 in credit reports, third‑party services, lead generation, and internal labor on each loan that fell out. The industry is effectively burning hundreds of billions of dollars of application volume and hundreds of millions of dollars of expense each year.

Against that backdrop, increasing lender profitability by 15–20 basis points is achieved by reducing fallout 3-5%. It starts with treating pull‑through improvement as a disciplined, data‑driven process that any lender can manage—then using agentic AI to automate and scale that process.

Step 1: Make fallout visible in your pipeline

Most lenders glance at lock pull‑through weekly or monthly, but the real leverage comes from seeing fallout risk at the loan level, in near real time. A practical internal process looks like this:

- Define your stages: RESPA application taken, file complete, underwritten, approved with conditions, clear‑to‑close, funded.

- For each stage, calculate historical pull‑through (what percent of loans in that stage actually funded) by product, channel, loan officer, and rate environment.

- Build simple rules that flag at‑risk loans, such as: no borrower contact in 5+ days, conditions outstanding past a set threshold, a lock near expiration without clear‑to‑close, or a large pricing gap versus current market or competitors.

Simple spreadsheets and standard report help risk rate active loans by their likelihood of fallout and the financial impact if they do. That alone shifts the conversation from “How big is our pipeline?” to “Which loans are we in danger of losing this week?”

Step 2: Diagnose why borrowers leave

Because most fallout is the borrower choosing to go elsewhere or they stop the process, your next task is to understand those choices. “Withdrawn” means the borrower withdraws, fails to provide information so the loan is closed for incomplete information, “ghosts” the lender, etc. Internally, that means:

- Standardizing reasons for withdrawal and decline in your LOS or CRM (rate/fees, property issues, documentation fatigue, timing, personal circumstances).

- Conducting short, structured post‑mortems on lost loans—especially purchase loans and larger balances—to determine the real drivers.

- Comparing fallout patterns by loan officer, branch, and channel.

By mapping these patterns to your fallout data, you can design specific interventions: training, process changes, or targeted pricing flexibility.

Step 3: Turn insight into daily action

Operationalize this into a daily routine: Segment the list by action required:

- Loans needing immediate MLO outreach.

- Loans where secondary should consider pricing or lock strategy changes.

- Loans where operations leadership should remove internal bottlenecks.

- Provide simple, recommended actions for each segment: call scripts, email templates, condition‑clearing checklists, or escalation paths.

- At week’s end, review which at‑risk loans were saved and which were lost, and refine your rules accordingly.

Even done manually, this process tends to improve pull‑through because it focuses attention on the right loans at the right time, instead of treating the pipeline as a flat list. Each “saved” loan means a huge boost in profit: Gain on sale of $5,000-14,000 versus lost cost of $2,000 or more.

Step 4: Where Agentic AI fits

The challenge with a manual approach is bandwidth. This is where agentic AI changes the game—by doing what a disciplined analyst or sales manager would do, but continuously and at scale:

- Apply your rules and learned patterns to score each loan’s pull‑through probability.

- Detect early warning signals you might miss: rising silence from the borrower, repeated rate‑shopping behavior or milestone stagnation.

- Draft tailored actions for each role—MLO, secondary, sales leader, finance—so people can act immediately.

- Learn from outcomes: when an intervention saves a loan, it reinforces that pattern; when it fails, the model adjusts.

Conceptually, agentic AI is just an automated version of the disciplined process a lender could run by hand. That is precisely why it works: it encodes your best practices, then executes them tirelessly on every loan, every day.

Step 5: The profitability impact

When only 59% of RESPA applications become funded loans, every incremental improvement in pull‑through represents a large pool of “found” profitability:

- The lender generate the full gain on sale and fees earned on a closed loan, as opposed to writing off the costs of the withdrawn loan.

- Hedge performance improves because actual pull‑through improves.

- You capture more servicing and relationship value from borrowers who might otherwise have drifted away.

For many lenders, that combination is worth 15–20 basis points of P/L improvement.

And declinations can be handled in a similar fashion with agentic AI.

Bringing it together (and how Teraverde helps)

Any lender can start this journey today with the tools they already have. As those practices mature, agentic AI is a scalable engine that executes the process continuously.

Teraverde has packaged this approach into a pre‑built agentic AI solution that plugs into existing systems and reflects these best practices out of the box. For lenders who want the benefits of disciplined pull‑through management and agentic automation—without building everything from scratch—Teraverde’s agent provides a ready‑to‑deploy solution increase profit and reduce fallout.

James M. Deitch

James M. Deitch serves as co-founder and CEO of the Teraverde group of companies. Teraverde , founded in 2011, develops analytics products such as Coheus® and provides strategy consulting to financial services companies. Prior to Teraverde, Deitch founded two national banks, several mortgage banking ventures, and four technology-oriented companies. Jim is a frequent speaker, industry thought leader and best-selling author. He is working on his fourth book, “Disruptive AI: It’s Coming to You or For You” to be published in Spring 2026. LinkedIn URL https://www.linkedin.com/in/james-m-deitch-cpa-cmb/ Company URL www.coheus.com

Ready to Grow and Scale Your Operations?

Gain unparalleled efficiency, compliance, and insights with Loan Vision. Begin your journey with us today.

Microsoft Certified Partner

.png)